Failing to prepare a comprehensive tax strategy is a quick way to turn your retirement into a not-so-rosy picture. Taxes impact retirees in many ways, but with the recent passage of the “One Big Beautiful Bill” (OBBBA), many of the favorable tax brackets we’ve enjoyed are now permanent.

This adds certainty to your planning, but it also confirms that the “tax gap” between ordinary income and capital gains is here to stay—making Net Unrealized Appreciation (NUA) more relevant than ever. You should coordinate each piece of your income stream to create a proactive strategy, and for those with company stock, NUA is a powerful tool to evaluate.

If you have been granted stock from your employer, congratulations! You likely received employer stock over many years. Your shares of company stock are only one piece of your total retirement assets. The first step most people take after retirement is rolling over their 401k to a Rollover IRA. In the rollover process, you liquidate the investments you held in your 401k. In your new Rollover IRA, you select your new investments that fit your risk tolerance and retirement distribution plan. But wait, not so fast, you can’t forget about the company stock!

Know the rules

When you hold company stock in your 401(k), the IRS sees that value in two separate parts:

- The Cost Basis: This is what the stock was worth when it was first added to your account (the “original price”).

- The NUA: This is the growth.” The difference between that original price and what the stock is worth today.

Normally, when you take money out of a 401(k) or IRA, the IRS taxes the entire amount as ordinary income (up to 37%).

The NUA strategy changes the game. By following specific rules, you can “rescue” that growth from high income tax rates. Instead of paying 37% on the whole balance, you pay income tax only on the original price (basis). The growth, the NUA, is taxed at the much lower long-term capital gains rate (usually 15% or 20%) only when you sell it.

Which path to take?

At retirement (or even when you change employers), you essentially have two options to consider for your company stock. The first option is to roll it over into a Rollover IRA with the rest of the assets. The second option is that you could distribute the company stock to a brokerage account and roll the rest of your assets into a Rollover IRA.

Why would anyone take the latter? Let’s tackle the bad news first. The latter sounds complicated, and you’d be facing a tax bill right away. Well, the tax bill might not be as large as you’d think. You would be liable for income tax on only the cost basis of your employer stock. Then, you may continue to hold the stock indefinitely in the brokerage account.

Moving to the good news. Once you decide to sell the company stock, you would only be facing capital gains tax on the NUA and any additional gains since you moved the stock to the brokerage account. The NUA tax savings could make any analysis to determine the best strategy for your company stock very much worthwhile.

Taking advantage of NUA is amplified when your company stock has a low-cost basis. With a low-cost basis, NUA allows you to take a limited tax hit now on just the basis instead of paying income tax rates on the entire position later.

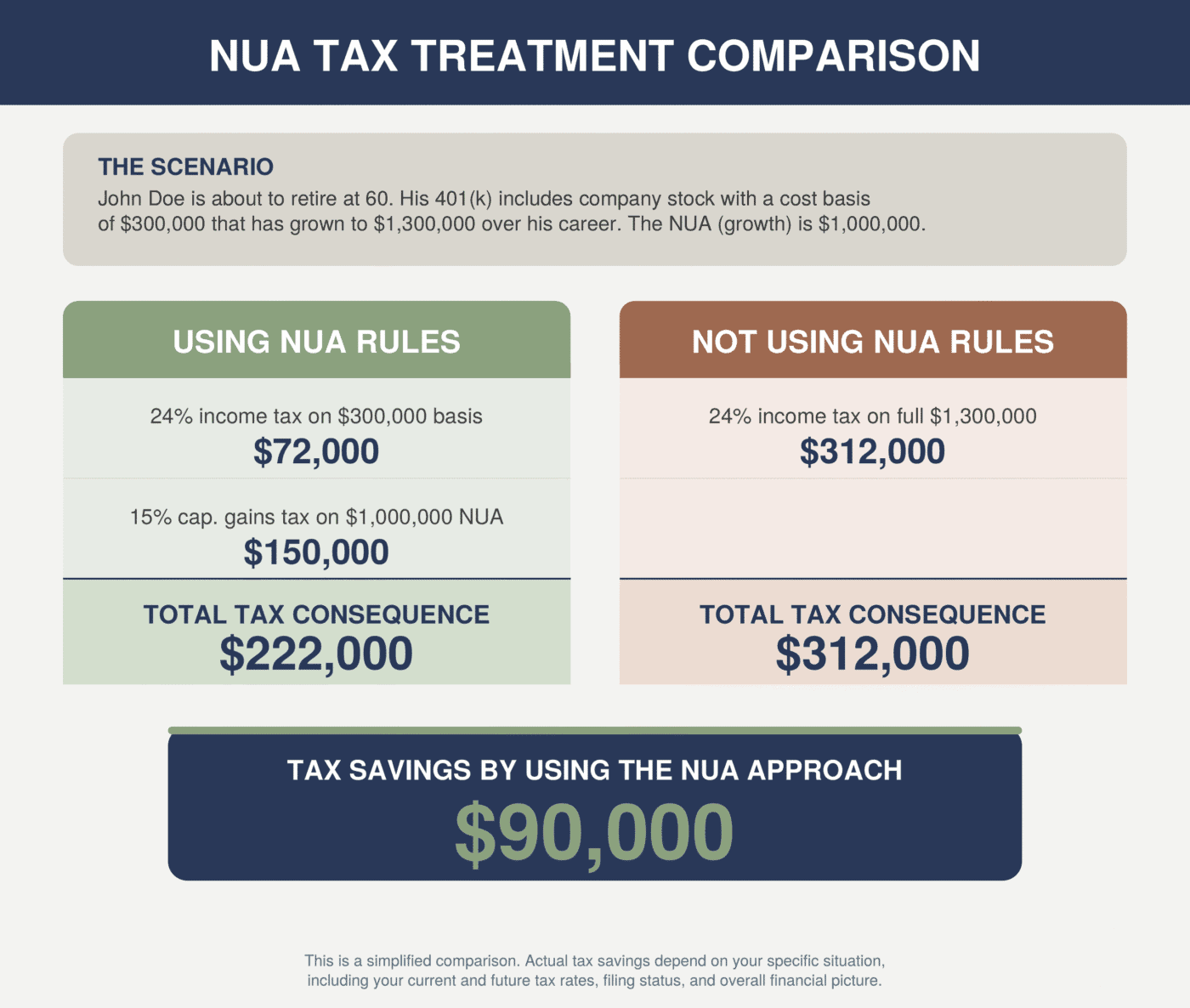

Let’s take a look at an example. John Doe is about to retire at 60. His 401(k) balance includes company stock. The cost basis of that stock is $300,000 and has grown over his career to $1,300,000.

⚠️ Two Rules You Can’t Afford to Miss

NUA is a “one-shot” opportunity. If you miss a step, the IRS generally won’t let you “un-ring the bell.”

- Rule #1: The All-or-Nothing Requirement: To qualify, you must perform a Lump-Sum Distribution. This means you must empty the entire balance of your 401(k)—not just the stock—within a single calendar year. If you leave even $1 in the account past December 31st, you could void the NUA treatment for the stock.

- Rule #2: The Early Withdrawal Penalty: If you are under 59½ and haven’t separated from service after age 55, a 10% penalty applies to the cost basis portion ($300,000 in John’s case). The $1M NUA itself is exempt from the penalty, but that $30,000 extra tax bill on the basis is a significant factor.

John Doe has two options:

Using NUA tax treatment

John will distribute the stock from his 401(k) to a brokerage account. He will be subject to income tax rates on the $300,000 (cost basis). The gain of $1,000,000 would not be taxed yet.

When he decides to sell the stock in the brokerage account, he would be subject to capital gains rates on the $1,000,000 NUA and any additional appreciation since moving to the brokerage account.

There is a nuanced advantage for John’s estate. While the NUA portion itself ($1M) does not typically get a ‘step-up’ in basis (it’s considered Income in Respect of a Decedent), any additional appreciation that happens after the stock leaves the 401(k) does qualify for a step-up. Furthermore, because these are not IRA assets, John’s heirs aren’t forced into the strict 10-year RMD depletion rules that now apply to inherited IRAs under SECURE 2.0.

Not using NUA tax treatment

John will roll the entire balance of his 401(k) into a Rollover IRA. His assets would continue to grow tax-deferred. Once he begins to take distributions, the distributions will be taxed at ordinary income rates.

IRA assets do not offer a step-up in basis for beneficiaries. At John’s passing, there would be no step-up in basis in this scenario.

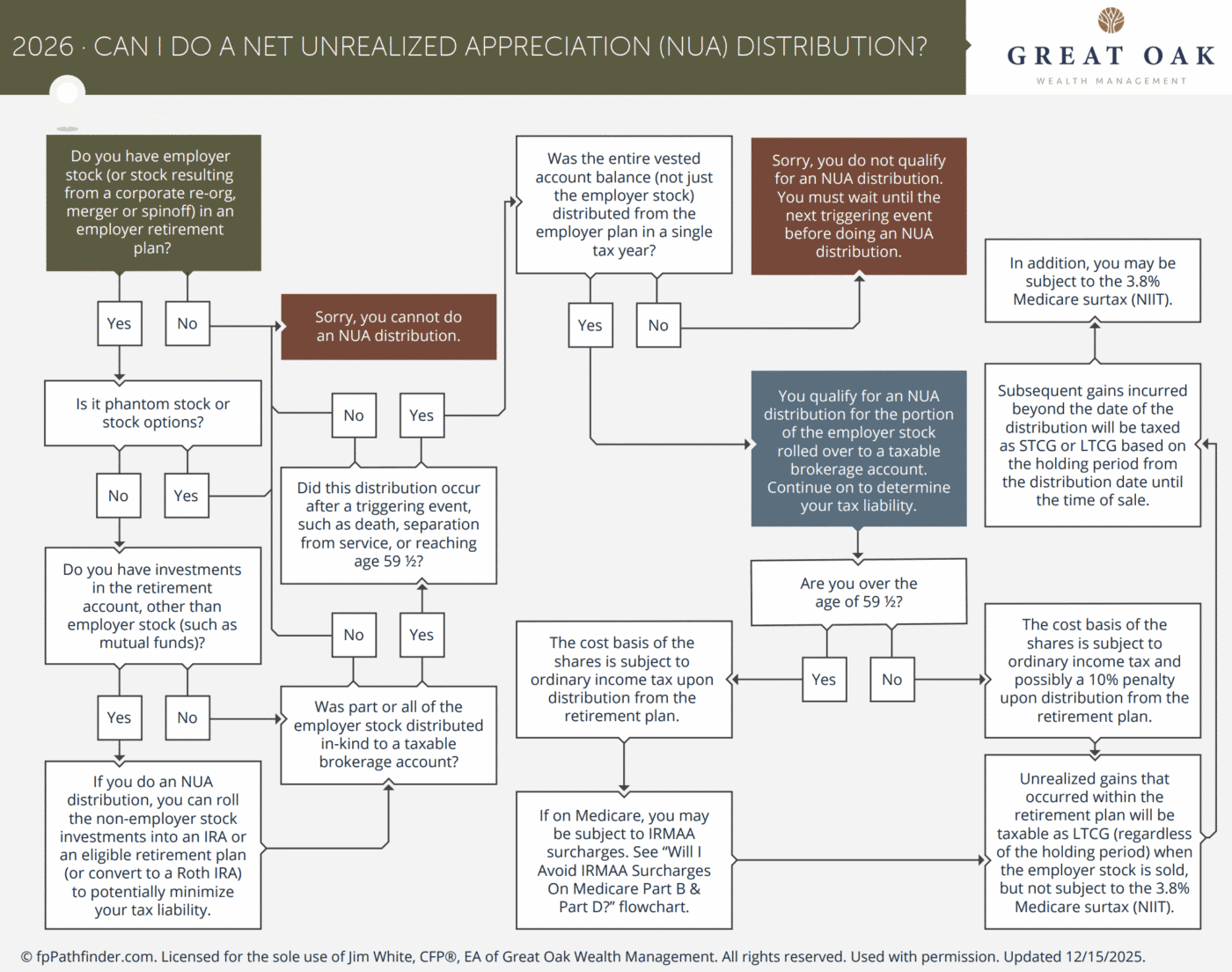

Here is a handy chart to help you determine if you can do an NUA distribution.

If your financial plan projects lower tax rates in retirement, NUA treatment will look less favorable the larger the balance of company stock you own relative to your total 401(k) balance. The key is to pause and evaluate whether to use NUA before moving any company stock in your 401(k), whether at retirement or when you are changing jobs. You could use the NUA tax treatment to realize meaningful tax savings, depending on your unique situation.

2026 Pro-Tip: If you are age 65 or older, the OBBBA introduced a new $6,000 Senior Bonus Deduction. This can be a great way to help offset the ordinary income tax you’ll owe on the cost basis of your stock in the year of distribution.

If you know someone who could benefit from this blog post, please pass it along to them using one of the ‘share’ buttons below!