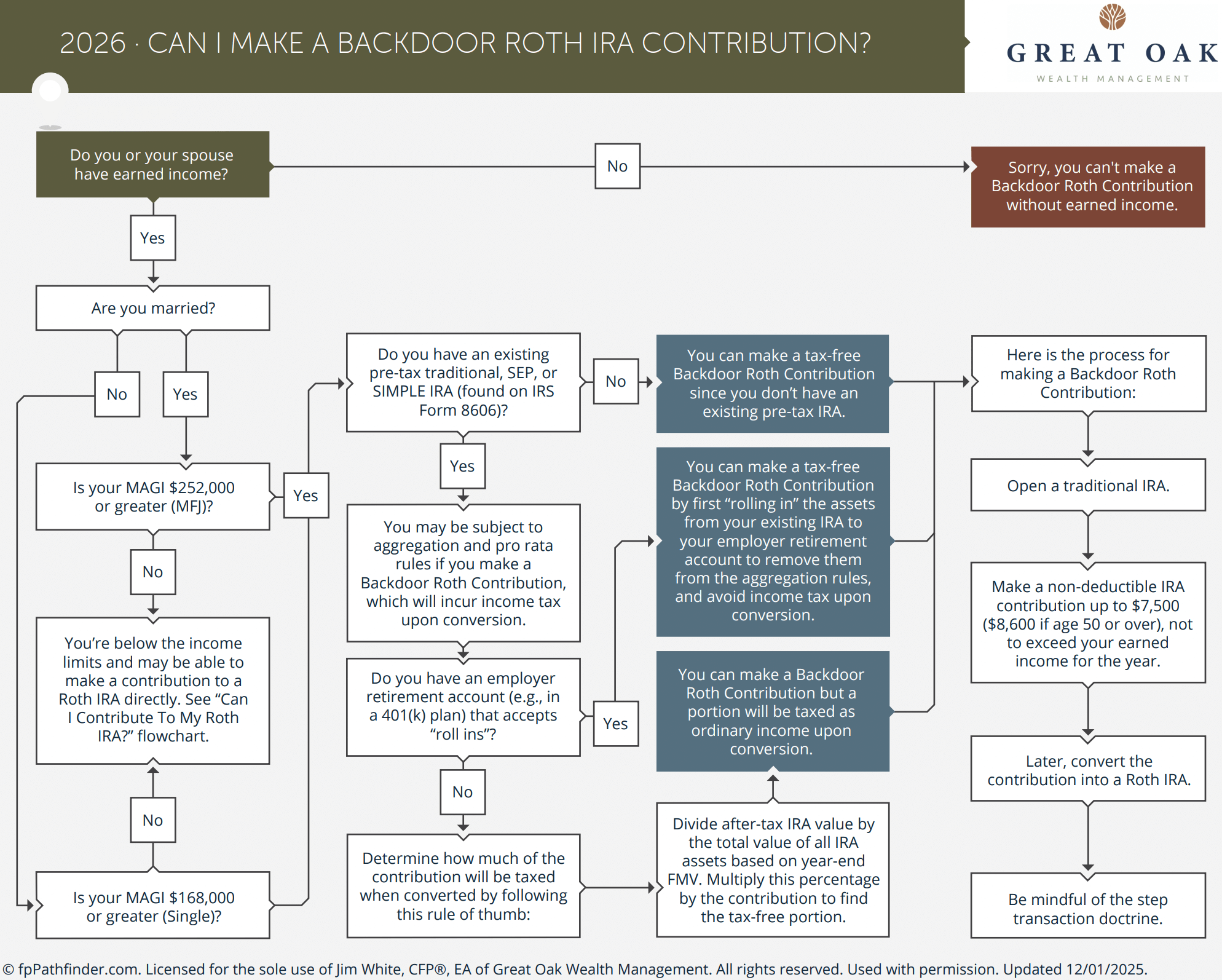

The backdoor Roth strategy is a sweet loophole in the tax code that allows individuals who would otherwise be disqualified from contributing to a Roth IRA to do so. Technically speaking, it’s not a Roth IRA contribution but a Roth IRA conversion. No matter what it’s called, the bottom line is if the backdoor Roth strategy is organized just right, it could provide a nice tax-free retirement wealth boost.

The Roth IRA Basics

You can contribute $7,500 (2026) per year or $8,600 if you are 50+. However, if your income is over the modified adjusted gross income phase-outs of…

…then you’re prevented from making any Roth IRA contributions.

You can make reduced Roth IRA contributions when your income falls within those phase-out ranges. The allowable contribution is reduced as you approach the $168,000 (S) or $252,000 (MFJ) limit.

Why consider a Backdoor Roth?

The backdoor Roth strategy allows high-earning households to circumvent those limits, providing the opportunity of annual Roth contributions and access to tax-free withdrawals after age 59½ with no required minimum distribution!!! Ever!!! You can let the Roth IRA sit untouched until the cows come home and pass it to your heirs. Unlike a traditional IRA, your heirs owe no taxes on an inherited Roth IRA.

Let’s call it what it is – a way to game the system legally. Yes, there is always the chance that the loophole could be closed, but the government has had plenty of opportunities to do so over the years but hasn’t. Yet.

What are the cons?

For each backdoor Roth IRA conversion you make, you must wait five years to withdraw those converted funds. Otherwise, you risk paying additional penalties on money that’s already been taxed.

But here’s the thing. To get the most significant benefit of the backdoor Roth, you must let it grow and increase your tax-free retirement income allocation. So tapping those funds soon after converting defeats the purpose of creating tax-free wealth!

The aggregation rule, which we’ll cover in more detail shortly, adds up all of your other traditional IRAs to determine how much of the backdoor Roth conversion will be tax-free.

When is the backdoor Roth appropriate?

You should consider the backdoor Roth if you check off the following boxes.

- You are maxing out your contribution to your employer’s 401k/403b.

- You max out contributions to a Health Savings Account if you’re eligible.

- Have a fully funded emergency fund.

- You have extra cash you would like to invest.

- Have little to no other traditional, SEP, or SIMPLE IRAs because of the aggregation rule

If you meet the above criteria, you are in the backdoor Roth sweet spot and let the tax-free fun begin. It’s a no-brainer.

Backdoor Roth Mechanics

How do you implement the backdoor Roth strategy? Will it be beneficial? Will it be 100% tax-free? All good questions. Let’s break this down.

Step #1 – Determine if you have any other traditional IRA accounts/balances.

Here is the most critical step and is often the make-or-break factor when deciding whether to do the Backdoor Roth. When we say Traditional IRAs, this includes Rollover, Traditional SEP, and Traditional SIMPLE IRAs.

Congratulations if you have no other Traditional IRAs, SEPs, or SIMPLE IRAs. The entire backdoor Roth will be tax-free. Pass Go, collect two hundred, and move on to the next step.

If, on the other hand, you have other Traditional IRAs, SEPS, or SIMPLEs, a calculation called the aggregation rule is required to determine how much of the backdoor Roth will be tax-free.

For example, let’s assume you have the following:

- Traditional IRA of $300,000

- SEP IRA with $100,00

We’ll also assume you haven’t read this blog post yet and decided to go ahead and implement the backdoor Roth strategy. You contribute $7,500 of non-deductible contributions to a Traditional IRA and convert those funds to a Roth IRA.

Since you have other IRAs, the IRS requires you to aggregate them and determine the tax-free amount of your conversion. Here are the steps:

- Add up the all of your IRAs $300,000 + $100,000 + $7,500 (yes, including the new non-deductible contribution)= $407,500

- Divide the non-deductible contribution by the total IRA amount: $7,500/$407,500 = 1.84%

- Multiply $7,500 x 1.84% = $138 is the non-taxable conversion amount

- $7,362 is the taxable conversion amount

The backdoor Roth is not very beneficial, with only $138 of the conversion tax-free. Those other IRAs are ruining the fun.

Don’t worry if it sounds confusing. Here is a handy-dandy flow chart.

What are your options?

Did you notice that nowhere in the aggregation rules mentioned anything about a 401k/403b? The aggregation rule only aggregates IRAs. If you can roll over all of your other IRAs into your 401k, that removes them from the aggregation calculation. Let’s be clear: if you have a 401k with high fees and limited investment choices, doing this may not be the best move. It comes down to weighing the benefits versus the disadvantages.

Keep on keep’in on with Non-deductible contributions. Maybe the backdoor Roth strategy is not in the cards due to your current tax rate and the aggregation rule. That’s ok. If you’re maxing out your retirement savings and still want to save more in a tax-deferred manner, maybe you should keep on making annual non-deductible contributions. All growth and earnings grow tax-deferred. The two points you need to understand are regarding the withdrawals.

- Non-deductible contributions are subject to RMDs, just like any other IRA, and

- The aggregation rule previously mentioned also applies to withdrawals to determine the distribution’s taxable versus non-taxable amount.

- It may be appropriate for Roth Conversions in the future.

Entire Roth Conversion: Maybe it’s in your best long-term tax interest to convert all your IRAs to Roths, clearing the deck and allowing for 100% tax-free backdoor Roth conversion every year. There are many variables to consider in this decision – age, income, tax brackets, both now and projected in retirement, and the amount of your traditional IRA, SEP, or SIMPLE balances. This move requires much more analysis and may even be counterproductive from a tax perspective. Check out our blog post, Learn how to Implement a Roth Conversion Effectively to learn more, or better yet, contact us BEFORE you make that move.

If you and your trusted advisor determine that the backdoor Roth strategy is for you, it’s time to move on to the next steps.

Step #2 Open a Traditional IRA

Make your annual contribution. Remember you have until the tax filing deadline to make IRA contributions for the previous year.

Step #3 Open a Roth IRA

You or your advisor must process the Roth conversion, moving the funds from the traditional IRA to the Roth IRA, which typically requires some paperwork.

One note: the conversion is based on a calendar year. So, if you contribute to your 2025 IRA on March 15, 2026, the contribution is reported on your 2025 tax return. If you immediately convert that to a Roth, it gets reported on your 2026 tax return.

Step #4 -Record the transaction when you file taxes

The non-deductible IRA contribution and Roth conversion transactions are reported on Form 8606 of your tax return. You’ll notice the aggregate questions and calculations on lines six through thirteen.

Step #5 Wash-Rinse-Repeat

If you can, keep using the backdoor Roth strategy every year until it doesn’t make financial sense, i.e., when your earned income decreases below the phase-out level, enabling regular Roth IRA contributions, you are subject to the aggregation rule, or the loophole is closed.

Last word

A backdoor Roth conversion can make a lot of sense for individuals and households seeking to access tax-free funds in retirement. However, the aggregation rule can be tricky to calculate, so it’s essential to carefully weigh the potential costs relative to the anticipated benefits BEFORE you implement the backdoor Roth strategy.

We hope you enjoyed this post. Consider signing up for our monthly newsletter if you’d like to read more. You can do so via the sign-up form below.